Is American Electric Power Company (AEP) a Buy?

AEP is overvalued when above $98 and undervalued at $79. At its current price of around $74, the company is likely to be undervalued with an estimated two-year return of 21%.

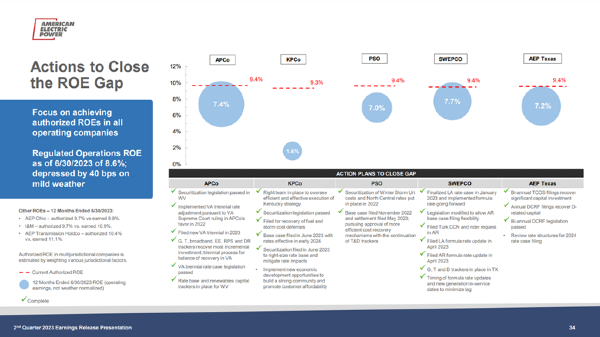

There are risks with investing in AEP. Return on Equity (ROE) has so far fallen short of expectations. Across the company’s multiple holdings, the target ROE was 9.3% or higher. The range of ROE for their portfolio of utilities was around 7.4% in Q2 2023 with their Kentucky holdings an outlier with an abysmal 1.6% ROE.

Return on equity measures how efficiently the utility is using the company’s equity to make a return for shareholders without further security issuance or debt. As AEP is effectively a regulated utility, the ROE is regulated by commission boards in their respective jurisdictions.

Many of their jurisdictions have authorized returns in the range of 9% to 11%. The actual returns for these jurisdictions were in line with the authorized ROEs set by regulators.

AEP’s other risk is their miss on funds from operations (FFO) to total debt. Current FFO/debt stands at 11.1% while the target is 14% to 15%. This miss was questioned multiple times from different angles on the Q2 2023 conference call. Analysts wanted to know a plan of action to get back to the target and when.

If neither of these metrics improve by the company’s Q4 2023 earnings call, expect continued stagnation in AEP’s stock price as institutional investors sour on AEP’s prospects. However, there were reasonable signs on the conference call that the team has a plan of action to meet their targets.

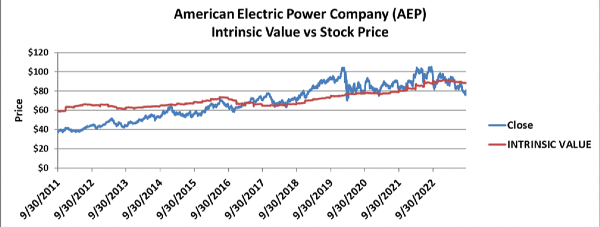

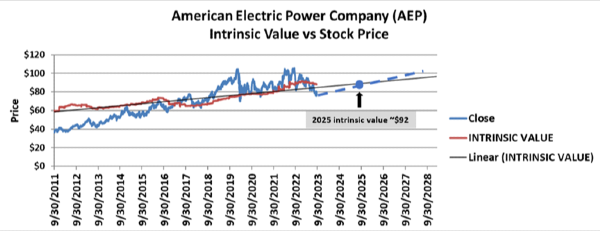

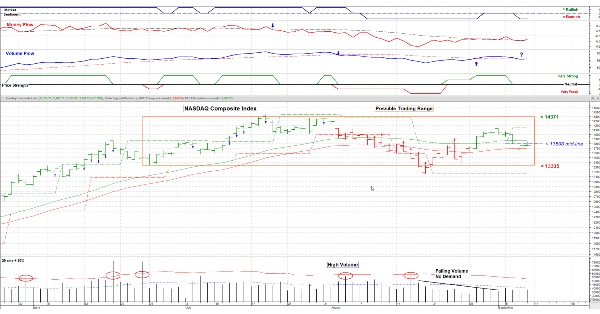

AEP intrinsic value versus stock price

AEP Price Target

AEP’s two-year price target is $92. This price target expects AEP to meet its annual operating earnings goal of 6% to 7% growth. Earnings per share were lower year over year, with weather a key item blamed for the negative growth. The team reaffirmed they will meet their earnings growth goals for 2023. Earnings growth is a key to turn around a falling intrinsic value. If intrinsic value continues falling, it could detrimentally affect the price target.

Why is AEP Falling?

AEP is falling because its intrinsic value has fallen in the last few quarters due to stagnated EPS growth and falling book value per share. The market placed a risk factor on AEP, allowing the price to fall below its intrinsic value, something that hasn’t occurred since 2016.

Interest rates are taking a toll on AEP’s price on two fronts. First, the company is getting hit by higher interest costs, directly affecting earnings. Getting control of FFO to total debt will help elevate earnings erosion caused by interest payments. Higher interest rates also affect intrinsic value, as we must discount earnings even higher as interest rates have gone up.

AEP must get operating earnings growth to hit 6% to 7% target this year or risk losing more faith from the market.

Read More: How to Value a Utility stock

Will AEP Stock Split?

AEP stock will not split in the foreseeable future and hasn’t had a stock split in the last 30 years. AEP is keen on maintaining its dividend, which dampens price growth.

Typically, splits are made to make stock prices reasonable for retail investors and to provide lower price ranges for option contracts. AEP, by its nature, isn’t a high growth stock and doesn’t have a highly active options market for its underlying asset versus other growth stocks like Tesla or Google. Hence, it’s very unlikely that AEP will conduct a stock split in the next decade.

Is American Electric’s Dividend Safe?

American Electric’s dividend is not entirely safe. There are headwinds that the company needs to pass through in the short run.

In the long run, AEP’s dividend is safe and will continue growing. Population and company migration out of AEP’s territory could hurt its dividend in the long run, but this is unlikely as Texas and some other Southern states with high population growth are in AEP’s territory.

Changes to how utilities are regulated could have a major impact on the utility’s dividend. AEP is going all-in as a regulated utility. This gives the company an effective monopoly on power generation, transmission, and distribution in their territories. However, if more states continue to deregulate their utilities, then AEP will have to change their strategy which could put its dividend at risk.

In the short term, AEP needs to meet their balance sheet targets and reduce their cost of credit. These costs are eroding earnings. Their dividend policy is 60% to 70%. Hence, to keep the dividend growing, they need to meet their operating earnings growth targets.

Is American Electric Power Great for Retirees?

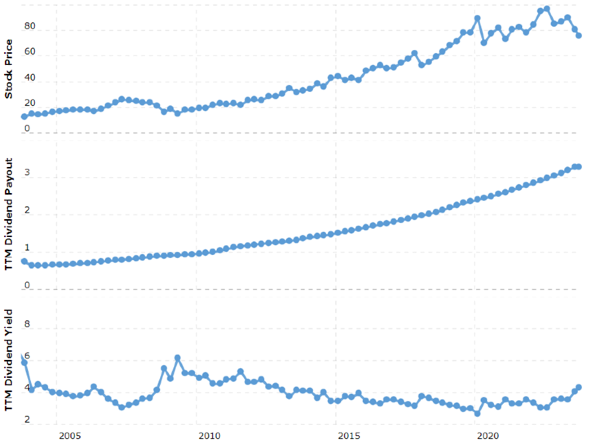

AEP is a great long-term investment for retirees. AEP’s dividend has consistently grown since 2001.

The stock’s dividend is protected due to AEP being a regulated utility. Their effective monopoly and regulated earnings rate allow them to receive consistent earnings from their capital equipment.

AEP’s dividend policy is in line with other successful utilities. Finally, the territories they provide power to are mostly growing in terms of population and economic activity. This should all help to continue growing the company into the future.

AEP News that Could Affect the Stock Price

The executive team at AEP is determined to shed its unregulated business assets so that the company can simplify its business and focus on being a regulated utility. Their ability to sell these assets have had mixed results.

The sale of their Kentucky operations failed to come to fruition. This deal would have helped further strengthen AEP’s balance sheet. Instead, they now have to contend with an operating segment with an abysmal 1.6% ROE.

Regardless of the Kentucky deal, AEP continues to divest away from unregulated assets. In August, AEP completed the sale of a renewable energy holding that represented 1,200 MW of wind and 165 MW of solar in 11 states. For the sale, AEP earned $1.2 billion in cash. The proceeds will be used to focus on building up AEP’s core business as a regulated utility.

Is AEP a Good Investment?

AEP is a good investment for income investors and dividend growth investors. The stock is also a great investment to investigate if you’re a value investor.

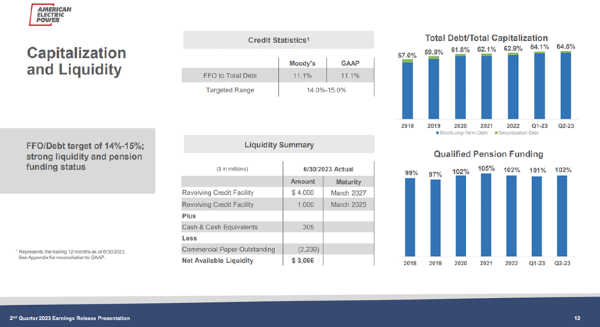

AEP is great for these investors due to its consistent, but moderate, growth of revenue, earnings, and dividends. But the stock isn’t perfect, as its total debt to total capitalization is creeping higher. This is again causing an erosion of AEP’s earnings that the executive team is actively responding to.

As a potential stock for value investors, AEP has a proven track record of consistency. The stock has had consistent eps and revenue growth that aligns with the stock selection guide’s mantra of up, straight and parallel.

AEP Earnings Growth

Earnings growth is at risk for 2023, but the executive team is confident they can get growth back on track in the coming quarters. Earnings growth could be strengthened or hindered by the following:

- Mild weather. The executive team leaned heavily into mild weather as a cause for the earnings miss. Expect this to be reversed as hotter temperatures in the summer will likely cause an increase in A/C use. This should be reflected in the Q3 results.

- Interest payments. FFO to total debt is still low at 11.1%. This needs to get up to 14% to reduce the interest erosion on EPS.

- Revenue growth. Not discussed as much on the Q2 2023 call was revenue. This was good as the executive team focused on company problems like debt and eroded earnings. However, though revenue fell year-over-year, it’s still on a positive long-term trajectory.

- Close the ROE gap. The executive team needs to find ways to close the ROE gap on some of their operating units. Their focus on effective “re-negotiations” with regulators is a right step in closing this gap.

Overall, the price forecast reflects no additional risk factor placed on earnings this quarter. However, if the 3rd quarter does not show improvement towards the target, a risk factor will be added to earnings.

AEP Book Value

AEP has had a consistent upwards trend of book value over the last decade; however, book value per share has recently stagnated. The company needs to continue growing earnings so that they can pay their dividend and reinvest in the company. The latter should start growing book value.

Book value will continue to flounder as the executive team reorganizes their energy portfolio and sells off assets to align their company to be a pure play regulated utility company. This is fine long term as the focus on a core competency should allow AEP to improve earnings and use capital more effectively.

The FFO/debt goal is 14 to 15 percent, but right now it sits at 11.1%. The company is converting certain assets into cash to meet this goal and is targeting early 2024 to reach this metric. In the meantime, the sell-off of assets will place uncertainty on the book value of the company.

Our price forecast considers a 5% risk factor on AEP’s book value.

Read More: Why do Utilities have a High Debt-to-Equity Ratio?

Setting a Risk Factor for American Electric

Overall, the market hasn’t placed a risk factor on AEP. However, AEP’s price recently fell below its intrinsic value for the first time since 2016 as the market gauges how risky AEP’s portfolio movements are. Our price forecast places a 20% risk factor on top of AEP’s intrinsic value to set the undervalued price point.

When calculating intrinsic value, we set a 5% risk factor on AEP’s book value as the company is taking systematic steps to strategically sell assets. Once the sells are complete, we’ll assess if the 5% risk factor should be removed.

AEP Stock Forecast

We expect AEP stock to continue growing through the decade and even into 2040. The company is looking to invest more into renewable energy, which will de-couple AEP from the volatility of the energy markets.

AEP 2025 Stock Forecast

AEP’s two-year price target is $92. This price target assumes intrinsic value will rebound and continue its multi-year trajectory.

AEP Five-year Stock Forecast

Expect continued, tempered growth through the decade with a 2028 price target of $102. The growth will likely stay mute as earnings are distributed as dividends.

Read More: AEP analysis in Q1 2023

I/we have a position in an asset mentioned

Is American Electric Power Company (AEP) a Buy?

AEP is overvalued when above $98 and undervalued at $79. At its current price of around $74, the company is likely to be undervalued with an estimated two-year return of 21%.

There are risks with investing in AEP. Return on Equity (ROE) has so far fallen short of expectations. Across the company’s multiple holdings, the target ROE was 9.3% or higher. The range of ROE for their portfolio of utilities was around 7.4% in Q2 2023 with their Kentucky holdings an outlier with an abysmal 1.6% ROE.

Source: AEP Q2 2023 investor presentation

Return on equity measures how efficiently the utility is using the company’s equity to make a return for shareholders without further security issuance or debt. As AEP is effectively a regulated utility, the ROE is regulated by commission boards in their respective jurisdictions.

Many of their jurisdictions have authorized returns in the range of 9% to 11%. The actual returns for these jurisdictions were in line with the authorized ROEs set by regulators.

AEP’s other risk is their miss on funds from operations (FFO) to total debt. Current FFO/debt stands at 11.1% while the target is 14% to 15%. This miss was questioned multiple times from different angles on the Q2 2023 conference call. Analysts wanted to know a plan of action to get back to the target and when.

If neither of these metrics improve by the company’s Q4 2023 earnings call, expect continued stagnation in AEP’s stock price as institutional investors sour on AEP’s prospects. However, there were reasonable signs on the conference call that the team has a plan of action to meet their targets.

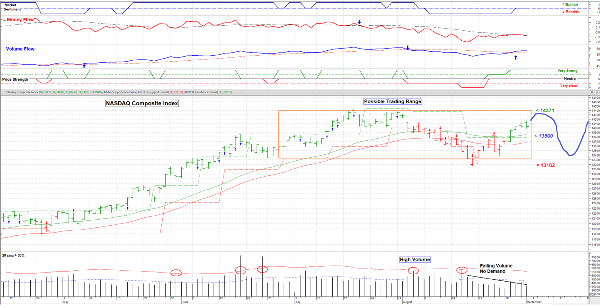

AEP intrinsic value versus stock price

AEP Price Target

AEP’s two-year price target is $92. This price target expects AEP to meet its annual operating earnings goal of 6% to 7% growth. Earnings per share were lower year over year, with weather a key item blamed for the negative growth. The team reaffirmed they will meet their earnings growth goals for 2023. Earnings growth is a key to turn around a falling intrinsic value. If intrinsic value continues falling, it could detrimentally affect the price target.

Why is AEP Falling?

AEP is falling because its intrinsic value has fallen in the last few quarters due to stagnated EPS growth and falling book value per share. The market placed a risk factor on AEP, allowing the price to fall below its intrinsic value, something that hasn’t occurred since 2016.

Interest rates are taking a toll on AEP’s price on two fronts. First, the company is getting hit by higher interest costs, directly affecting earnings. Getting control of FFO to total debt will help elevate earnings erosion caused by interest payments. Higher interest rates also affect intrinsic value, as we must discount earnings even higher as interest rates have gone up.

AEP must get operating earnings growth to hit 6% to 7% target this year or risk losing more faith from the market.

Will AEP Stock Split?

AEP stock will not split in the foreseeable future and hasn’t had a stock split in the last 30 years. AEP is keen on maintaining its dividend, which dampens price growth.

Typically, splits are made to make stock prices reasonable for retail investors and to provide lower price ranges for option contracts. AEP, by its nature, isn’t a high growth stock and doesn’t have a highly active options market for its underlying asset versus other growth stocks like Tesla or Google. Hence, it’s very unlikely that AEP will conduct a stock split in the next decade.

Is American Electric’s Dividend Safe?

American Electric’s dividend is not entirely safe. There are headwinds that the company needs to pass through in the short run.

In the long run, AEP’s dividend is safe and will continue growing. Population and company migration out of AEP’s territory could hurt its dividend in the long run, but this is unlikely as Texas and some other Southern states with high population growth are in AEP’s territory.

Changes to how utilities are regulated could have a major impact on the utility’s dividend. AEP is going all-in as a regulated utility. This gives the company an effective monopoly on power generation, transmission, and distribution in their territories. However, if more states continue to deregulate their utilities, then AEP will have to change their strategy which could put its dividend at risk.

In the short term, AEP needs to meet their balance sheet targets and reduce their cost of credit. These costs are eroding earnings. Their dividend policy is 60% to 70%. Hence, to keep the dividend growing, they need to meet their operating earnings growth targets.

Is American Electric Power Great for Retirees?

AEP is a great long-term investment for retirees. AEP’s dividend has consistently grown since 2001.

Source: macrotrends.net

The stock’s dividend is protected due to AEP being a regulated utility. Their effective monopoly and regulated earnings rate allow them to receive consistent earnings from their capital equipment.

AEP’s dividend policy is in line with other successful utilities. Finally, the territories they provide power to are mostly growing in terms of population and economic activity. This should all help to continue growing the company into the future.

AEP News that Could Affect the Stock Price

The executive team at AEP is determined to shed its unregulated business assets so that the company can simplify its business and focus on being a regulated utility. Their ability to sell these assets have had mixed results.

The sale of their Kentucky operations failed to come to fruition. This deal would have helped further strengthen AEP’s balance sheet. Instead, they now have to contend with an operating segment with an abysmal 1.6% ROE.

Regardless of the Kentucky deal, AEP continues to divest away from unregulated assets. In August, AEP completed the sale of a renewable energy holding that represented 1,200 MW of wind and 165 MW of solar in 11 states. For the sale, AEP earned $1.2 billion in cash. The proceeds will be used to focus on building up AEP’s core business as a regulated utility.

Is AEP a Good Investment?

AEP is a good investment for income investors and dividend growth investors. The stock is also a great investment to investigate if you’re a value investor.

AEP is great for these investors due to its consistent, but moderate, growth of revenue, earnings, and dividends. But the stock isn’t perfect, as its total debt to total capitalization is creeping higher. This is again causing an erosion of AEP’s earnings that the executive team is actively responding to.

As a potential stock for value investors, AEP has a proven track record of consistency. The stock has had consistent eps and revenue growth that aligns with the stock selection guide’s mantra of up, straight and parallel.

AEP Earnings Growth

Earnings growth is at risk for 2023, but the executive team is confident they can get growth back on track in the coming quarters. Earnings growth could be strengthened or hindered by the following:

Source: AEP investor relations

Overall, the price forecast reflects no additional risk factor placed on earnings this quarter. However, if the 3rd quarter does not show improvement towards the target, a risk factor will be added to earnings.

AEP Book Value

AEP has had a consistent upwards trend of book value over the last decade; however, book value per share has recently stagnated. The company needs to continue growing earnings so that they can pay their dividend and reinvest in the company. The latter should start growing book value.

Book value will continue to flounder as the executive team reorganizes their energy portfolio and sells off assets to align their company to be a pure play regulated utility company. This is fine long term as the focus on a core competency should allow AEP to improve earnings and use capital more effectively.

The FFO/debt goal is 14 to 15 percent, but right now it sits at 11.1%. The company is converting certain assets into cash to meet this goal and is targeting early 2024 to reach this metric. In the meantime, the sell-off of assets will place uncertainty on the book value of the company.

Our price forecast considers a 5% risk factor on AEP’s book value.

Setting a Risk Factor for American Electric

Overall, the market hasn’t placed a risk factor on AEP. However, AEP’s price recently fell below its intrinsic value for the first time since 2016 as the market gauges how risky AEP’s portfolio movements are. Our price forecast places a 20% risk factor on top of AEP’s intrinsic value to set the undervalued price point.

When calculating intrinsic value, we set a 5% risk factor on AEP’s book value as the company is taking systematic steps to strategically sell assets. Once the sells are complete, we’ll assess if the 5% risk factor should be removed.

AEP Stock Forecast

We expect AEP stock to continue growing through the decade and even into 2040. The company is looking to invest more into renewable energy, which will de-couple AEP from the volatility of the energy markets.

AEP 2025 Stock Forecast

AEP’s two-year price target is $92. This price target assumes intrinsic value will rebound and continue its multi-year trajectory.

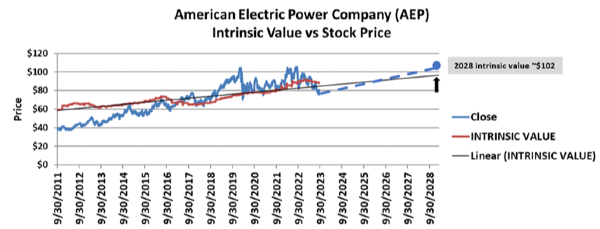

AEP Five-year Stock Forecast

Expect continued, tempered growth through the decade with a 2028 price target of $102. The growth will likely stay mute as earnings are distributed as dividends.